Discovering that your insurance settlement falls short of your actual repair costs can easily add frustration to an already difficult situation. The damage to your home was stressful enough and now the company you’ve been paying premiums to for years is offering a fraction of what you actually need to make things right.

This situation is more common than most Florida homeowners realize. Understanding why it happens and what options exist can really make a significant difference in the outcome.

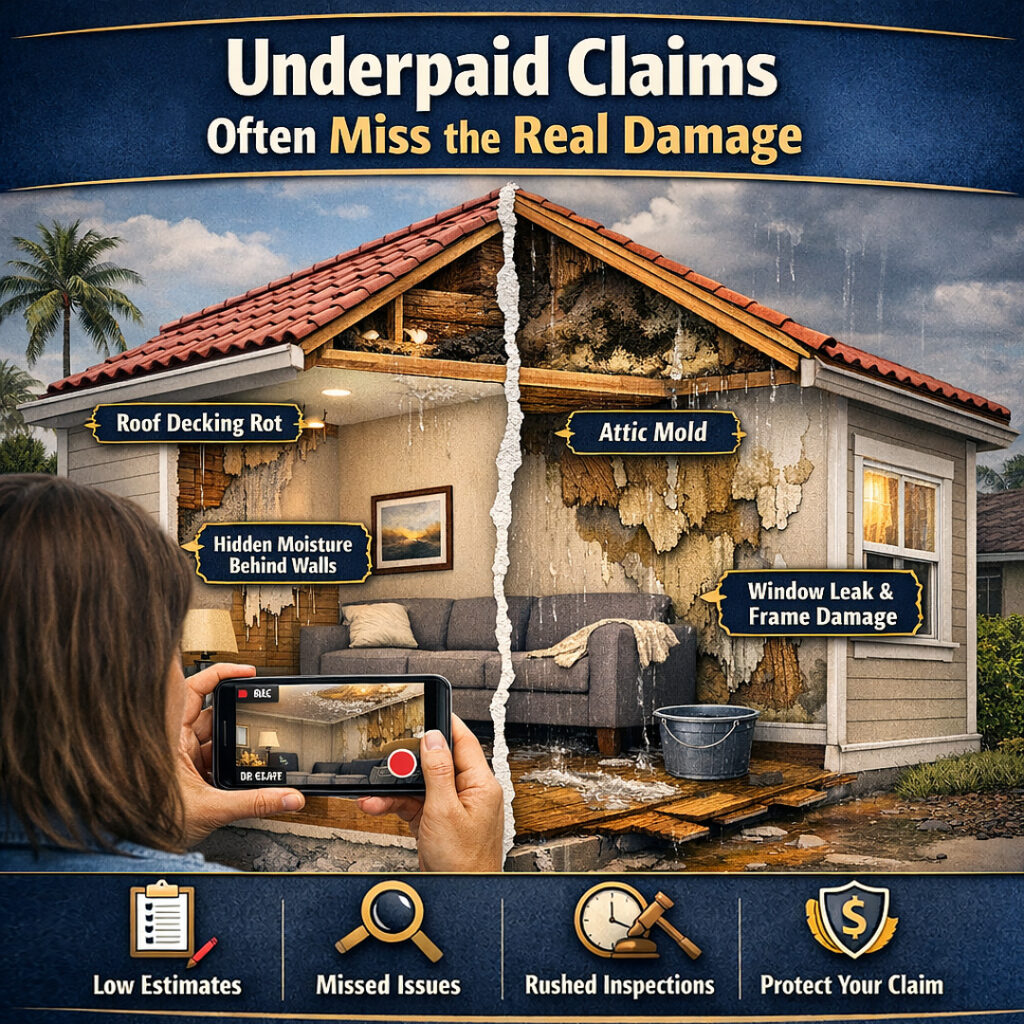

Insurance settlements sometimes fall short of actual repair costs for reasons that have little to do with the legitimacy of the damage itself. Several factors can contribute to this:

Outdated Cost Estimates – Some insurers base their calculations on repair costs from previous years rather than current 2026 pricing. With construction costs rising, especially in Florida where demand for contractors remains high, this approach can result in settlements that don’t fully reflect what repairs actually cost today.

Overlooked Damage – Initial assessments sometimes miss hidden issues. Water damage behind walls, structural compromises that aren’t immediately visible, or secondary damage that developed after the initial loss can all go unaccounted for in a quick walk-through inspection.

Disputes Over Cause – Insurance companies may attribute damage to causes not covered under the policy. A common example involves claiming that hurricane damage was actually due to flooding (which usually requires separate coverage) or suggesting that roof damage existed before the storm.

Depreciation Calculations – Policies differ in how they handle depreciation. Some homeowners discover their settlement is based on “actual cash value” rather than “replacement cost,” meaning the insurance company deducted for age and wear even though replacing the damaged item costs full price.

The First Offer Isn’t Always Final – Many people assume the initial settlement check represents the insurance company’s final decision. In reality, that first offer can often be reconsidered.

Before depositing a settlement check or signing any release forms, it’s worth taking time to review the estimate carefully. Comparing the insurance company’s numbers against actual contractor quotes for the same work can reveal significant gaps. If the settlement doesn’t align with what repairs will genuinely cost, there may definitely be room for negotiation.

Documentation Makes a Difference

When challenging an insurance company’s valuation, evidence becomes crucial. The strength of a dispute often comes down to how well the damage and repair costs can be substantiated.

Helpful documentation typically includes:

This documentation doesn’t just support a homeowner’s position, it makes it harder for insurance companies to justify offering less than what the evidence is clearly demonstrating.

Florida’s Legal Framework

Florida has specific laws governing how insurance companies must handle claims, including timeframes for responding to claims and standards for how losses should be calculated. When these requirements aren’t met, or when settlements don’t reflect the actual scope of damage, legal options may be available.

Property damage attorneys who focus on insurance disputes understand these regulations and how they apply to individual situations. They can review settlement offers, identify where insurance companies may have undervalued claims, and handle negotiations that homeowners might not feel equipped to manage on their own.

When Professional Help Makes Sense

Not every settlement dispute requires legal intervention. Minor discrepancies might be resolved through direct communication with the insurance company or by providing additional documentation.

However, certain situations often benefit from professional legal assistance:

In these scenarios, having someone familiar with Florida insurance law and experienced in these disputes can level the playing field.

Moving Forward

Receiving an underpaid settlement doesn’t mean accepting it as final. Florida homeowners have rights when it comes to insurance claims, and those rights include the ability to challenge valuations that don’t accurately reflect their losses.

The process can sometimes feel overwhelming, especially when dealing with property damage at the same time. But understanding that options exist and that help is available and can make the situation feel less insurmountable.

Call us today!

We represent homeowners, business owners, contractors, restoration and mitigation professionals, in their disputes against the insurance companies.

Phone : (786) 786-9633

Email : office@finmanlawgroup.com

2514 Hollywood Blvd, Suite 502

Hollywood, FL 33020